A job-order costing system that relies on normal costing will. At the beginning of the year a company estimated that 20000 direct labor-hours would be required for the periods estimated level of production.

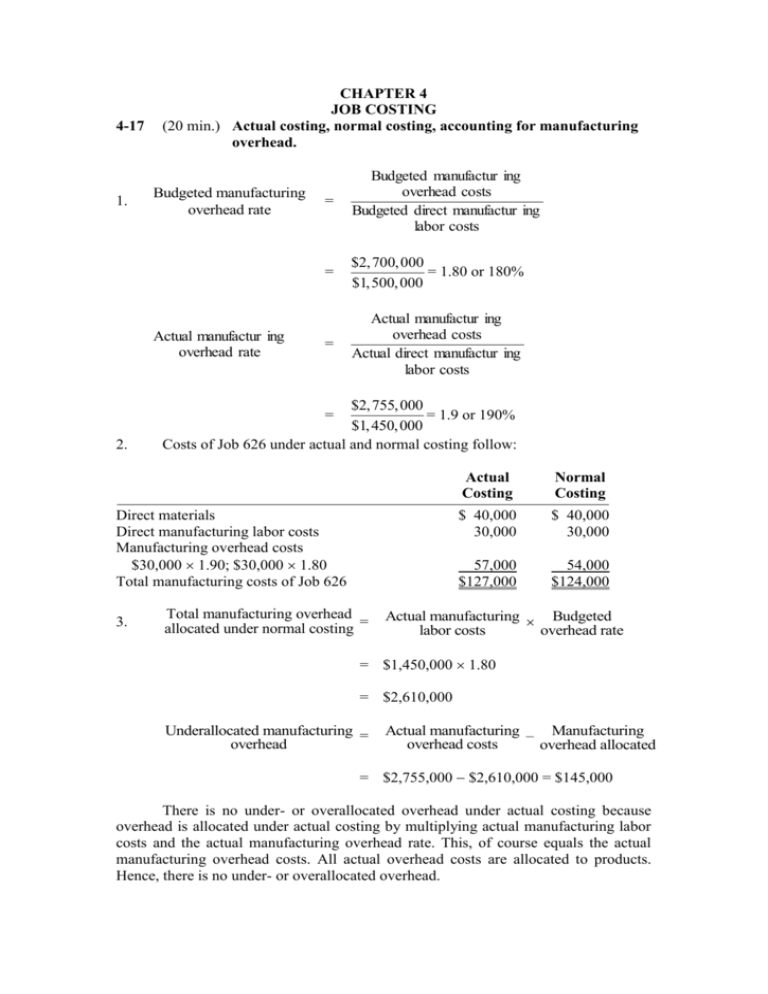

Chapter 4 Job Costing 4 17 20 Min Actual Costing Normal

Every business needs a way to track how much it costs to develop its products or deliver its services which in turn helps the business determine how to price the products and services for profitability.

. Job costing or job order costing is the costing method in which company allocates variable and production overhead cost to the individual job. What is a job order costing system. This system determines the price of each individual product and ensures that the cost for each product is reasonable enough for a customer to purchase it while still allowing the company to make a profit.

Work in Process Inventory accounts. In a business applying job order costing each job or order is assigned a job number to distinguish it from the others. Estimated total manufacturing overhead cost in the numerator.

The job order costing system is a costing method that is used to calculate the costs attached to an individual job or order. Job order costing and process costing are systems of collecting and allocating costs to units of production. To understand the flow of costs in job order costing system we shall consider a single months activity for a company a producer of product A and product BThe company has two jobs in process during April the first month of its fiscal year.

Exercise 5 Journal entries T Accounts Over and Under applied overhead Income Statement. Payroll records from which the hours worked on a specific job are charged to that job. Is ABC costing process costing.

Process cost systems have a Work in Process Inventory account for each department or process. Supplier invoices from which only those line items pertaining to a job should be charged to that job. What is a normal costing system.

Job costing example. The Precast Department recorded 3950 machine hours in November. The actual costing system like the name implies is a costing system that traces direct and indirect costs to a cost object by using the actual costs incurred in the job.

Apply overhead cost to Jobs by multiplylng an actual overhead rate by the estimated amount. Although this system is much more simplistic actual costing systems are not commonly found in real-world situations because actual costs cannot. Exercise 1 Cost accumulation Procedure Determination.

Assign actual direct materlals and direct labor costs to jobs. Apply overhead cost to jobs by multiplying an actual overhead rate by the actual amount of the. The differences between the two systems are shown in Table 51.

While each job represents a unit or a batch of products. The per unit cost formula is given below. F204 Chapter 5 Job Order Costing 30 Applied overhead in each department.

The job order costing system is used when the various items produced are sufficiently different from each other and each has a significant cost. Exercise 2 Job order cost sheet. Per unit cost Total cost applicable to job Number of units in the job.

The company also estimated 140000 of fixed manufacturing overhead cost for the coming period and variable. A job-order costing system that relies on normal costing will. Information Tracked by a Job Order Costing System.

Job 1 of 1000 units of product A was started in march. Assign actual direct materials and direct labor costs to jobs. 30 Billed the state of Nebraska for the completed.

Job order costing is a system that takes place when customers order small unique batches of products. Apply overhead cost to jobs by multiplying an actual overhead rate by the estimated amount of the allocation base incurred by the jobs. A job-order costing system that relies on normal costing will.

Job Order Costing System Exercises and Problems. Exercise 4 Job Order Cycle Entries. A job order costing system can be quite complex.

Process costing is a type of costing system used for production of. Assign actual direct materials and direct labor costs to jobs. A job-order costing system that relies on normal costing will.

It is a basic costing method which is applicable where work consists of separate projects or contract jobs. Features of job costing. Multiple Cholce Apply overhead cost to Jobs by multiplying a predetermined overhead rate by the estimated amount of the allocation base Incurred by the jobs.

Job cost systems have one Work in Process Inventory account for each job. Along with accurately recording costs by contract timely job costing is essential. Using job costing the cost of each job is.

While each job represents a unit or a batch of products. When cost allocation is done in a timely manner management is able to make decisions on jobs on an ongoing basis. The key difference between job order costing and process costing is that job costing is used when products are manufactured based on customer specific orders whereas process costing is used to allocate costs in standardized manufacturing.

When a companys output consists of continuous flows of identical low-cost units the process costing. Costs related to each job are allocated directly to each specific job. As we learned job order costing assigns costs to specific units or products.

Job order costing is extensively used by companies all over the world. A process cost system process costing accumulates costs incurred to produce a product according to the processes or departments a product goes through on its. A job order costing system accumulates the costs associated with a specific batch of products or services.

Definition of job costing. Assign actual direct materials and direct labor costs to jobs. Job order costing or job costing is a system for assigning and accumulating manufacturing costs of an individual unit of output.

Normal costing is used to derive the cost of a. The similarities between job order cost systems and process cost systems are the product costs of materials labor and overhead which are used determine the cost per unit and the inventory values. It must track information from multiple sources including the following.

Depreciation was recorded on equipment 18350. Without timely job costing management could miss an opportunity to identify unforeseen cost overruns that may require a change order to be applied. June 21 2021 by Martin Luenendonk.

One type of job-order costing is called actual costing. As we saw there are two traditional costing methods that companies use to assign costs to the products andor services that they provide. The per unit cost of a particular job is computed by dividing the total cost allocated to that job by the number of units in the job.

Job order costing and process costing. Exercise 3 Job order costing-T Accounts and Journal Entries. Job costing is a costing method used to determine the cost of specific jobs which are performed according to the customers specifications.

A predetermined overhead rate includes.

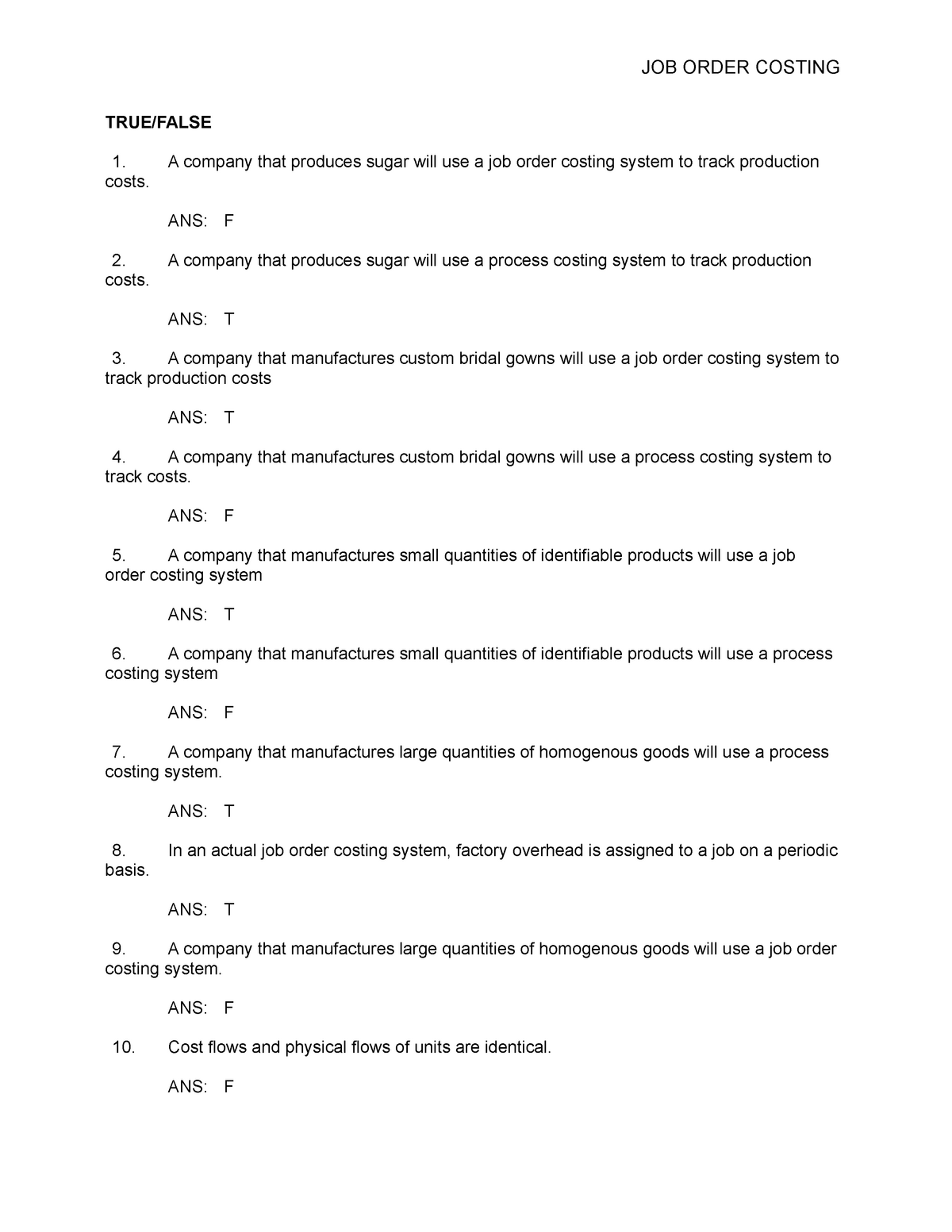

Job Order Costing Multiple Choices True False A Company That Produces Sugar Will Use A Job Order Studocu

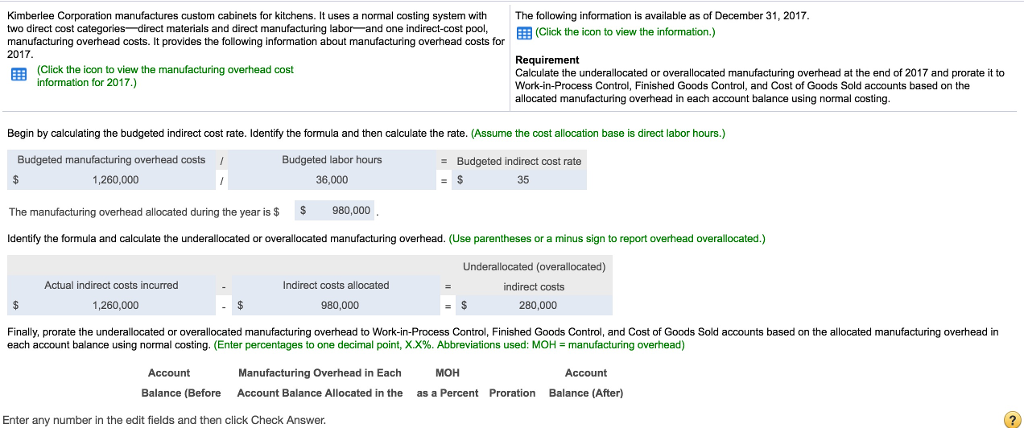

Solved Kimberlee Corporation Manufactures Custom Cabinets Chegg Com

Understand Cost Accounting Systems Input Measurement Actual Normal Standard Costing Inventory Valuation Thi Cost Accounting Check And Balance Accounting

0 Comments